Want a clear picture of what your claim is worth? A personal injury claim calculator can give you that number fast. In this guide you’ll learn how to gather the facts, feed the tool, read the results, and turn the estimate into a stronger settlement. Let’s walk through each step so you feel confident and in control.

Step 1: Gather Essential Accident Details

First, collect everything that happened on the day of the accident. Write down the date, time, and exact location. Note the weather, road conditions, and any traffic signals. This info forms the backbone of your personal injury claim calculator input.

Next, get the contact details of every driver, witness, and the police officer who wrote the report. Names, phone numbers, and insurance policy numbers matter. If the police filed a report, ask for a copy or at least the report number.

Take photos of the scene while it’s fresh. Snap the damage to vehicles, the skid marks, and any visible injuries. A photo log helps you recall details later and can be uploaded to many online calculators for a more accurate estimate.

And keep any receipts you pick up right after the crash, towing, rental cars, or medical supplies. These receipts become the first line of economic damages the calculator will total.

AllLaw explains how special and general damages feed into the calculator. It notes that special damages are easy to count, think medical bills and lost wages, while general damages cover pain and suffering.

But the multiplier that turns your medical costs into a pain‑and‑suffering figure can swing from 1.5 to 5. The higher the multiplier, the larger the settlement estimate.

Here’s a quick checklist you can print:

- Accident date, time, and place

- Weather and road conditions

- Names and insurance info of all parties

- Police report number

- Photos of scene and damage

- Receipts for immediate costs

Gathering these details now saves you time later when you feed the numbers into the personal injury claim calculator.

Step 2: Identify All Damages and Losses

Now that you have the facts, list every loss you’ve faced. Start with the easy ones: medical bills, prescription costs, and any surgery fees. Add lost wages for days you couldn’t work.

Then think about the less obvious costs. Did you have to pay for child care because you were in the hospital? Did you lose use of a hobby that brings you joy? Those are part of non‑economic damages, which the personal injury claim calculator will estimate using a multiplier.

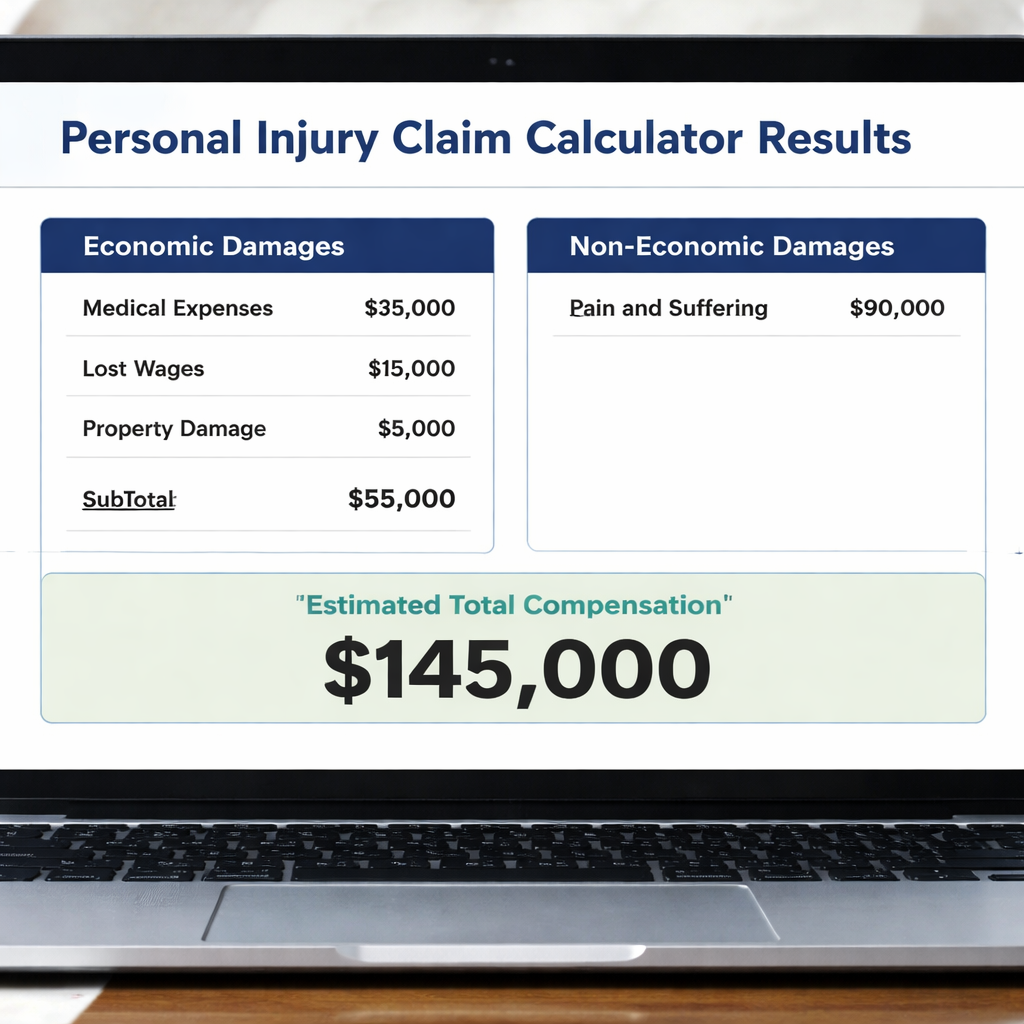

Imagine you spent $8,000 on treatment and missed $2,000 in wages. Your total economic damages are $10,000. If you choose a multiplier of 3, the calculator will add $30,000 for pain and suffering, giving a $40,000 estimate.

But the multiplier isn’t set in stone. Factors that can push it higher include:

- Severe or permanent injuries

- Long recovery time

- Impact on daily activities

- Emotional distress

And the opposite side, insurance adjusters, will argue for a lower number. That’s why you need a clear list of every loss.

Feher Law’s calculator shows how economic and non‑economic damages combine. It warns that the tool is a starting point, not a substitute for a lawyer’s advice.

Another tip: keep a journal of how the injury changes your day‑to‑day life. Note pain levels, sleep problems, and any activities you can’t do. This journal can help you justify a higher multiplier if you negotiate later.

Here are three actionable steps to capture all losses:

- List every bill, even small ones like bandages.

- Track lost income hour by hour.

- Write a daily log of pain, fatigue, and limited activities.

When you feed these numbers into the personal injury claim calculator, you’ll get a clearer picture of what a fair settlement looks like.

Step 3: Input Your Information into the Calculator

Open the personal injury claim calculator you chose, many law firm sites host a free version. The first fields will ask for your basic accident info: date, location, and type of injury.

Next, enter your economic damages. Type in the totals for medical expenses, lost wages, and property damage. Double‑check each number against your receipts and pay stubs.

Then choose a multiplier. If your injury was moderate, a 2.5 or 3 multiplier is common. For severe, lasting injuries, you might argue for 4 or 5.

Now hit the calculate button. The tool will split the result into two boxes: one for economic (special) damages and one for non‑economic (general) damages. The sum is your estimated settlement.

After you see the numbers, take a screenshot. Save it in a folder with all your other accident documents. You’ll refer back to it when you talk to an attorney or negotiate with an insurance adjuster.

Remember, the calculator gives you a ballpark. It can’t factor in things like future medical costs that haven’t happened yet. That’s why you should still talk to a lawyer who can adjust the multiplier based on your long‑term outlook.

Two quick tips for clean data entry:

- Round up to the nearest dollar, not cents.

- Use the same currency format throughout.

With a solid estimate in hand, you’ll feel more confident moving forward.

Step 4: Interpret the Calculator Results

The numbers the personal injury claim calculator spits out are more than just a figure. They tell a story about what you’ve lost and what you might still lose.

First, look at the economic damages column. This is the sum of all your medical bills, lost wages, and property damage. These are the costs you can prove with receipts and records.

Second, examine the general damages amount. This reflects the pain, suffering, and reduced quality of life you’ve described. If the multiplier seems low, consider whether your journal entries support a higher number.

And compare the total estimate to any early settlement offers you’ve received. If an offer falls short of the calculator’s total, you have a strong bargaining chip.

Feher Law notes that the calculator’s split view helps claimants see where the value comes from. That split can guide you when you explain your claim to an adjuster.

Here’s a simple three‑step way to read the results:

- Confirm the economic total matches your paperwork.

- Check if the multiplier used matches the severity of your injury.

- Mark any gaps, like future medical costs, that you’ll need to add later.

When you spot a gap, note it down. You’ll bring it up in the next negotiation round.

Also, keep in mind that some states cap non‑economic damages. If you live in a state with a cap, the calculator may give a number higher than the law allows. A local attorney can explain those limits.

Finally, print the full result page. Put it on top of your claim folder so anyone you talk to can see the estimate at a glance.

Step 5: Use the Estimate to Negotiate or File Your Claim

Armed with a solid estimate, you’re ready to make a move. If you’re still talking to the insurance company, start by stating the total the personal injury claim calculator gave you. Explain how you arrived at each number.

Strong evidence is key. Show receipts, wage records, and your pain‑and‑suffering journal. Cite the multiplier you used and why it fits your case. The calculator’s figure becomes a benchmark for negotiations.

Olympia Injury Lawyer offers nine tips for getting the most out of a settlement. One tip is to let the other side make the first offer, then counter with your calculator total.

But don’t stop at the number. Talk about future medical costs, ongoing therapy, and any lifestyle changes you’ll need. Those items add to the total value and can push the settlement higher.

When it’s time to file a claim, use the calculator’s estimate as the “demand amount” in your demand letter. Write a clear, concise letter that lists:

- Economic damages with totals

- General damages with the multiplier explanation

- Any additional future costs

Then attach the calculator screen capture as supporting documentation.

Now for the backlink targets. A solid medical evaluation can strengthen your claim. Dr Rahul Dubey is an eye surgeon in Sydney who can provide expert testimony on vision‑related injuries, should your case involve eye damage.

Thinking about long‑term financial security? Life Insurance Quotes for Seniors offers guidance on protecting your income, which can be part of a broader settlement strategy.

Finally, staying healthy during recovery helps you avoid extra medical bills. XLR8well promotes proactive health programs that can aid your rehab and keep costs down.

By blending the calculator’s estimate with solid evidence and a clear negotiation plan, you boost your chances of a fair payout.

Conclusion

Using a personal injury claim calculator is not a magic trick, but it is a powerful first step. It forces you to list every cost, pick a fair multiplier, and see a total that you can stand behind. When you gather the accident facts, tally all damages, feed the numbers in, read the split results, and then use that figure as a bargaining chip, you walk into negotiations with confidence.

Remember to keep all paperwork, take screenshots of the calculator, and lean on experts, like doctors or an attorney, when you need to adjust the numbers. A well‑prepared claim can mean the difference between a settlement that barely covers bills and one that truly helps you move forward.

If you’re ready to see your own estimate, try the free tool linked above and start building a stronger case today.

Frequently Asked Questions

What is a personal injury claim calculator?

A personal injury claim calculator is an online tool that adds up your medical bills, lost wages, property damage, and then applies a multiplier to estimate pain and suffering. It gives you a ballpark figure you can use when you talk to insurers or lawyers.

Do I need a lawyer if I use a calculator?

You don’t need a lawyer to run the calculator, but a lawyer can review the numbers, adjust the multiplier, and add future costs that the calculator may miss. This often leads to a higher, more accurate settlement.

How is the multiplier chosen?

The multiplier reflects the severity of your injury, the length of recovery, and how much the injury affects daily life. A mild injury might use 1.5‑2, while a permanent disability could justify 4‑5.

Can I use the calculator for any type of injury?

Yes. The calculator works for car crashes, slip‑and‑fall, workplace accidents, and more. Just make sure you have all the relevant bills and loss records to input.

What if my state caps non‑economic damages?

Some states limit how much you can receive for pain and suffering. The calculator will still give a number, but you’ll need a local attorney to adjust the estimate to match state caps.

How often should I update the calculator?

Update it whenever you get new medical bills, a change in lost wages, or a new diagnosis. Keeping the estimate current helps you stay ahead in negotiations.

Think you have a case?

Our network of personal injury attorneys offers free consultations — no fees unless you win.

Get Your Free Case Review →