Want a fast, reliable ballpark figure for your personal injury claim? You can get that number in minutes, without paying a dime up front. In this guide we’ll walk you through everything you need to know about using a personal injury claim settlement amount estimator , from the factors that shape a settlement to the exact steps for gathering docs, crunching numbers, and knowing when to call a lawyer.

First, let’s see how the top three calculators stack up.

| Name | Covered Injury Types | Key Inputs Required | Estimation Methodology | Unique Feature | Best For | Source |

|---|---|---|---|---|---|---|

| Personal Injury Calculator | — | employment status, incident type, weekly pay, weeks missed, injury type, permanent impairment rating, age, future therapy/medications/surgery, scar details | based on data from thousands of past personal injury case settlements handled by Rob Levine Law | no personal information required to receive an estimate and includes a free consultation contact form | quick ballpark estimate for personal injury claim before speaking with an attorney | roblevine.com |

| New York Car Accident Settlement Calculator | car accident | medical expenses, lost wages, property damage, pain and suffering | calculates based on medical expenses, lost wages, property damage, and pain and suffering | free, instant calculation of potential settlement amount | quick ballpark figure for car accidents | rmfwlaw.com |

| Passenger Car Accident Settlement Calculator | car accident | medical expenses, lost wages, pain and suffering | — | — | — | theinjurylawyers.com |

Below we’ll break down each step you need to take, show you how to use the estimator tools, and explain why a free case review can keep you safe while you figure out your claim.

Understanding Settlement Factors

Before you type any numbers into a personal injury claim settlement amount estimator, you need to know what goes into the final figure. Settlements cover two broad buckets: economic damages and non‑economic damages.

Economic damages are the easy part. They’re the money you can point to on a receipt: medical bills, lost wages, property repair costs, and out‑of‑pocket expenses. Non‑economic damages are trickier. They cover pain, suffering, emotional distress, and loss of enjoyment of life. Because they’re subjective, insurers use formulas like a multiplier or per‑diem method to put a dollar value on them.

Key variables that can raise or lower your settlement include:

- Injury severity: A broken bone with a long recovery will fetch a higher multiplier than a minor sprain.

- Future medical needs: Ongoing therapy or surgery adds to both economic and non‑economic totals.

- Fault percentage: In comparative‑fault states, your award is reduced by your share of blame.

- Insurance policy limits: The at‑fault party’s policy caps what they can pay.

- Jurisdiction: Some states cap non‑economic damages by law.

Here’s what I mean: imagine you’re in a car crash in Massachusetts. You’ve got $5,000 in medical bills, you missed two weeks of work at $1,200 per week, and you’re dealing with a lingering back pain. Your economic damages total $7,400. If the lawyer suggests a multiplier of 4 for your pain and suffering, you add $29,600 (4 × $7,400) for non‑economic damages, landing at $37,000 before any fault reduction.

Why does this matter for a personal injury claim settlement amount estimator? Because most online tools let you plug in the basics (medical, wage loss) and then pick a multiplier range. Knowing how the multiplier works helps you choose a realistic number and not underestimate your claim.

We also need to keep an eye on tax rules. In most states, medical reimbursements aren’t taxed, but lost wages and punitive damages can be. That’s a detail you’ll want to confirm with a tax pro.

For a deeper dive on how Massachusetts comparative negligence works, you can read more on calculating a settlement in MA. This source explains the multiplier and per‑diem methods in plain language.

Gathering Your Accident Documentation

Any personal injury claim settlement amount estimator will ask for numbers. You can’t feed it data you don’t have. That’s why a solid document stack is the first thing you should collect.

Start with the obvious: police reports, medical records, and bills. Then add less‑obvious items like:

- Photographs of the scene, injuries, and damaged property.

- Witness statements with contact info.

- Employer statements confirming lost wages and any paid time off you used.

- Proof of ongoing expenses , e.g., receipts for prescription meds, therapy, or home‑care equipment.

- Insurance correspondence , claim numbers, adjuster letters, and any settlement offers.

All of these pieces help you fill in the fields of a personal injury claim settlement amount estimator accurately. For example, the estimator might ask for "weekly pay" , you’ll need recent pay stubs or a W‑2 to prove that number.

Here’s a step‑by‑step checklist you can follow:

- Request a copy of the police report within 30 days of the accident.

- Ask your doctors for a detailed treatment summary and a future care plan.

- Collect all medical invoices, even the ones marked "paid in full".

- Gather your most recent three pay stubs and your latest tax return.

- Save any emails or letters from the insurance adjuster.

- Take photos of your injuries every few days to track healing.

Why is this checklist vital? Because missing a single doc can cause an estimator to default to a lower number, which may lead you to accept a weak settlement offer.

Our free case review service can help you sort through this paperwork. You upload the docs securely, we match you with a local attorney, and they verify that nothing is missing before you even talk to an insurer.

Calculating Economic Damages

Economic damages are the "hard" numbers that you can prove with receipts. They’re the foundation of any personal injury claim settlement amount estimator.

Let’s break them down:

Medical Expenses

Include all costs from emergency care, hospital stays, surgery, prescription drugs, physical therapy, and any future medical procedures your doctor has recommended. Even over‑the‑counter meds count if you have receipts.

Lost Wages

Lost wages are calculated by multiplying your daily or hourly rate by the number of days you couldn’t work. For hourly workers, use your average hourly rate over the past 90 days. If you’re self‑employed, pull tax returns and bank statements to show average monthly earnings.

For example, if you earn $250 a day and missed 14 days, you’re owed $3,500. If you also used 3 days of PTO, add that value too.

Future Lost Earnings

If your injury reduces your earning capacity, you’ll need a projection. Work with a vocational expert to estimate how many years you can work, adjust for inflation, and discount to present value.

Property Damage

Repair estimates for your car, personal items, or any other property that was damaged. Get written quotes from at least two shops.

Out‑of‑Pocket Costs

Include things like transportation to medical appointments, home‑care services, and medical equipment rentals.

Putting it all together, here’s a simple spreadsheet you can use:

| Category | Amount |

|---|---|

| Medical Bills | $— |

| Lost Wages (past) | $— |

| Future Lost Earnings | $— |

| Property Damage | $— |

| Other Out‑of‑Pocket | $— |

Fill in each row with the numbers you gathered in the previous section. Then add them up , that’s your economic damages total, which you’ll plug into any personal injury claim settlement amount estimator.

Remember, the estimator you choose may ask for additional inputs like "permanent impairment rating" or "future therapy costs." Those come from your doctor’s report.

For a detailed look at how lost wages are calculated, see this guide on lost wages. It explains hourly vs. salaried calculations and how to handle self‑employment.

Using an Online Settlement Estimator (Video Walkthrough)

Now that you have your numbers, let’s see a real tool in action. Below is a video that walks you through the Personal Injury Calculator , the top pick from our research.

Watch the video, then pause at each step to enter your own data. The estimator will ask for:

- Employment status (full‑time, part‑time, self‑employed).

- Incident type (car crash, slip‑and‑fall, etc.).

- Weekly pay and weeks missed.

- Injury type and any permanent impairment rating.

- Age and future medical needs.

- Scar details, if any.

Because this tool does not collect personal data, you can use it safely on a public computer. After you hit "Calculate," you’ll see a quick ballpark figure and a link to a free consultation form , that’s the free case review we mentioned earlier.

Tip: Write down the estimate before you close the page. It’s a good reference point when you start negotiating with the insurer.

Comparing Estimator Outputs , A Quick Reference Table

Different calculators can give you different numbers. Here’s a quick way to compare the outputs you might see.

| Estimator | Economic Damages Input | Non‑Economic Method | Estimated Total | Notes |

|---|---|---|---|---|

| Personal Injury Calculator | Full economic data (medical, wages, property) | Database‑driven average multiplier | $— | Privacy‑first, no personal data needed |

| NY Car Accident Calculator | Medical, wages, property | Simple multiplier (1.5‑5) | $— | Fast, but only for car accidents |

| Passenger Car Calculator | Medical, wages | — (no methodology disclosed) | $— | Lacks transparency, no privacy statement |

When you see a big gap between estimates, ask yourself why. The Personal Injury Calculator pulls from thousands of past settlements, so it may give a more realistic range. The NY tool uses a generic multiplier, which can swing wildly.

Use this table as a checklist. If an estimator doesn’t ask for a key input you have, its result may be incomplete.

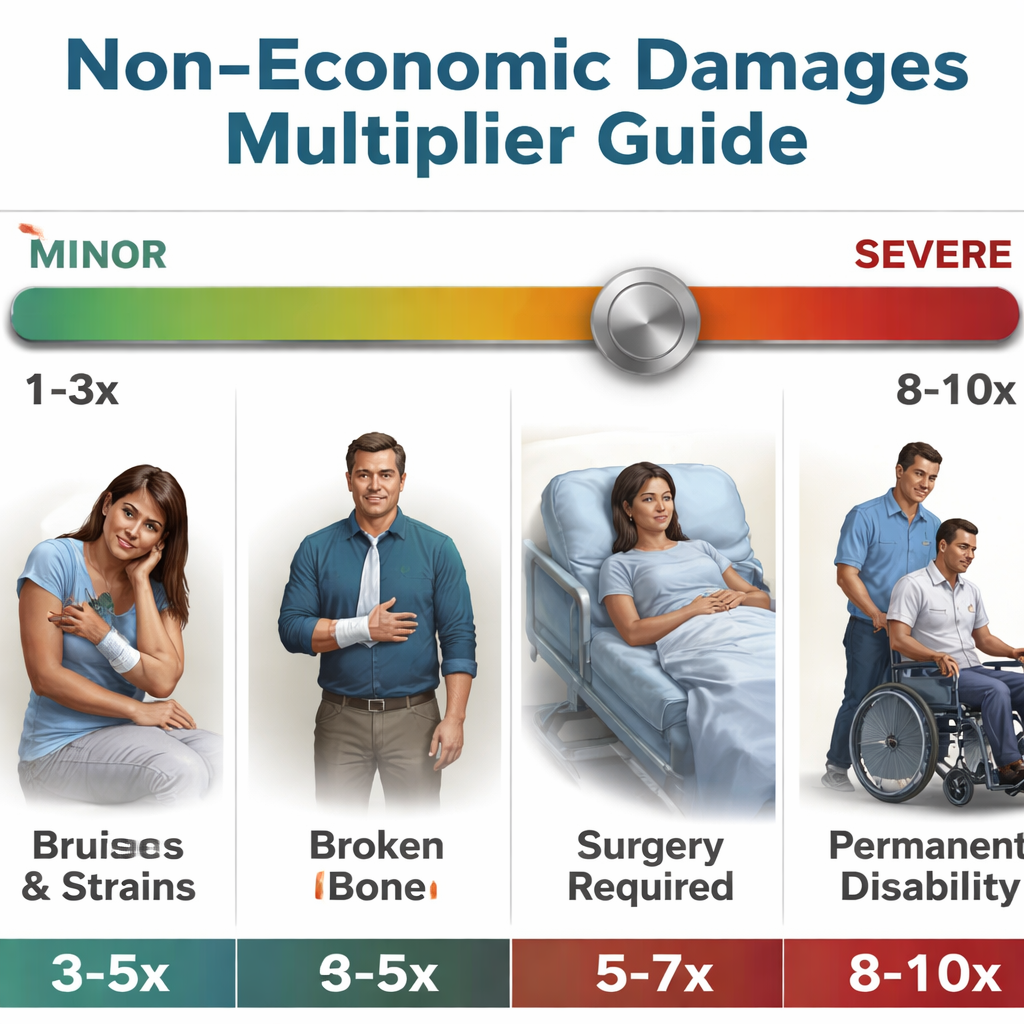

Adjusting for Non‑Economic Damages

Non‑economic damages cover the stuff you can’t put a receipt on , pain, anxiety, loss of enjoyment. Most estimators let you tweak a multiplier to reflect severity.

How to choose a multiplier:

- Minor injuries: 1.5 , 2.0

- Moderate injuries (fractures, surgery): 2.5 , 4.0

- Severe or permanent injuries: 4.5 , 5.0 or higher.

Factors that push you toward the higher end include:

- Long‑term therapy or rehab.

- Permanent scarring or disfigurement.

- Loss of a major life activity (e.g., inability to play sports).

- Significant emotional distress proven by a psychologist.

Here’s a quick visual aid to help you decide:

Remember, the multiplier is negotiable. During settlement talks, you’ll argue for the higher number while the insurer pushes for the lower one.

When to Seek Professional Legal Advice

Using a personal injury claim settlement amount estimator is a great first step, but you’ll hit a wall when the insurer starts low‑balling or when fault is disputed.

Hire a lawyer when any of these signs appear:

- Insurance offers less than 50 % of your estimator total.

- There’s a dispute over who caused the accident.

- Your injury is severe, permanent, or requires future medical care.

- You’re dealing with a large corporation or government entity.

- You need help gathering expert testimony (medical, vocational, economic).

Most personal injury attorneys work on a contingency basis , you pay nothing unless they win. That means you can get help without upfront costs.

Our free case review service matches you with a local attorney who can review your documentation, run a professional version of the estimator, and advise on next steps. The process takes about 24 hours after you submit your info.

For a deeper look at the South Carolina process, see this guide on hiring a personal injury lawyer. It explains the phases from discovery to trial.

Frequently Asked Questions

What is a personal injury claim settlement amount estimator?

A personal injury claim settlement amount estimator is an online tool that lets you input your economic and non‑economic loss data , like medical bills, lost wages, and injury severity , to get a ballpark figure of what your settlement could be. It’s a starting point for negotiations and helps you decide if an insurance offer is fair.

Do I need to give personal information to use an estimator?

Not all tools require personal data. In our research, the Personal Injury Calculator asks for no personal info, while the NY Car Accident Calculator asks for expense figures. Choose a privacy‑first option if you’re uncomfortable sharing details online.

How accurate are these estimators?

Estimators give a rough range. They can’t replace a lawyer’s detailed analysis, especially for future medical costs or complex liability issues. Think of the number as a conversation starter, not a final verdict.

Can I rely on the multiplier method for non‑economic damages?

The multiplier method is common and easy to understand, but the exact number is negotiable. A higher multiplier reflects more severe pain, longer recovery, or permanent loss. Use it as a guide, then discuss with an attorney to fine‑tune.

What if my insurance company offers a lower amount than the estimator?

That’s where a free case review helps. An attorney can compare the offer to your estimator total, point out missing expenses, and negotiate a higher figure. If negotiations stall, they can file a lawsuit.

How long does it take to get a settlement after filing a claim?

Timing varies. Simple cases can settle in a few weeks after a fair offer. More complex cases, especially with disputed fault or future medical needs, may take 6‑18 months or longer if they go to trial.

Do I have to pay any fees to use a personal injury claim settlement amount estimator?

No. The tools we reviewed are free to use. Our free case review also costs nothing , you only pay if you win, and then it’s a standard contingency fee.

What’s the statute of limitations for personal injury claims?

It depends on the state. Most states allow two years from the injury date, but some have shorter windows for government claims. A lawyer can confirm the deadline for your specific case.

Conclusion & Next Steps

Estimating your personal injury claim settlement amount is the first move toward getting the compensation you deserve. By understanding settlement factors, gathering solid documentation, crunching economic damages, and adjusting for non‑economic losses, you can walk into negotiations with confidence.

Remember: the estimator gives you a ballpark, not a guarantee. If the insurer’s offer feels low, or if your injury is serious, use our free case review to connect with a local attorney. They’ll review your numbers, protect your rights, and work on a contingency basis , meaning you pay nothing unless you win.

Take action now. Gather your docs, run the Personal Injury Calculator, and submit a free case review. The sooner you act, the stronger your claim will be before evidence fades or deadlines close.

Think you have a case?

Our network of personal injury attorneys offers free consultations — no fees unless you win.

Get Your Free Case Review →